Introduction

Spain’s property market entered 2026 with contrasting signals. While property sales declined at the start of the year, mortgage activity continued to expand, highlighting a complex dynamic between demand, financing conditions, and housing supply.

According to provisional data from the Spanish College of Registrars, the number of property transactions in January fell compared with the same month in the previous year. However, mortgage lending continued its upward trend, marking the nineteenth consecutive month of growth.

These figures reflect a market that remains active but is beginning to show signs of moderation following several years of strong growth.

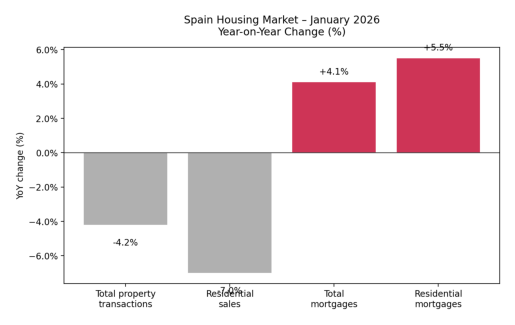

Key Market Data – January 2026 (Provisional)

| Indicator | January 2026 | Year-on-Year Change |

|---|---|---|

| Total property transactions | 113,600 | −4.2% |

| Residential property sales | 56,776 | −7.0% |

| Total mortgages | 50,800 | +4.1% |

| Mortgages on residential property | 40,087 | +5.5% |

| Mortgage growth streak | 19 consecutive months | — |

These figures highlight a divergence between transaction activity and financing, suggesting that although fewer homes were sold, access to credit remains strong.

A Decline in Property Transactions

Data from the registries shows that approximately 113,600 property sales were recorded in January 2026, representing a 4.2% decrease compared with January 2025.

When focusing specifically on residential properties, the slowdown becomes more pronounced. Around 56,776 home sales were registered during the month, reflecting a 7% year-on-year decline.

This marks the largest fall in housing transactions since mid-2024, suggesting the market may be entering a period of adjustment after several years of strong demand.

Several factors may explain the slowdown:

- Rising property prices across most regions

- Reduced affordability for first-time buyers

- Limited housing supply in key urban areas

- Longer negotiation periods between buyers and sellers

Despite these factors, analysts emphasize that the underlying demand for housing remains strong.

Mortgage Lending Continues to Expand

While transactions declined, mortgage lending maintained a strong trajectory.

In January 2026:

- 50,800 mortgages were constituted on all types of properties (+4.1% YoY)

- 40,087 mortgages were granted for home purchases (+5.5% YoY)

This marks nineteen consecutive months of growth in mortgage lending, suggesting financing conditions remain favorable.

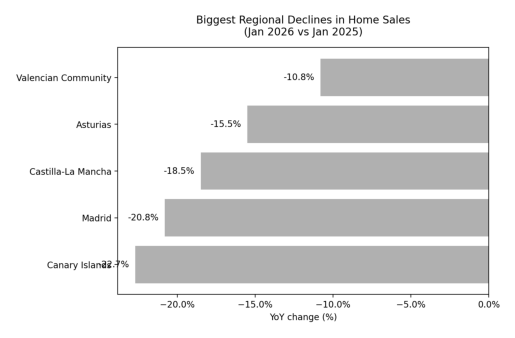

Year-on-Year Change in Residential Property Transactions by Autonomous Community

(January 2026 vs January 2025 – Provisional data from Registradores)

| Autonomous Community / City | YoY Change in Home Sales | Market Direction |

|---|---|---|

| Andalusia | −3.2% | Slight decline but still the highest transaction volume |

| Aragón | −11.7% | Moderate slowdown |

| Asturias | −15.5% | Significant decline |

| Balearic Islands | −6.4% | Slight contraction despite strong foreign demand |

| Basque Country | −5.1% | Moderate decline in a high-value market |

| Canary Islands | −22.7% | Largest regional drop in Spain |

| Cantabria | −4.3% | Mild contraction |

| Castilla-La Mancha | −18.5% | Major decline |

| Castilla y León | −7.9% | Moderate slowdown |

| Catalonia | −5.6% | Slight decline but still among largest markets |

| Community of Madrid | −20.8% | One of the steepest drops nationally |

| Valencian Community | −10.8% | Significant decline in coastal market |

| Extremadura | −2.1% | Market remains relatively stable |

| Galicia | −6.8% | Moderate decline |

| La Rioja | −8.4% | Small market contraction |

| Murcia | −3.9% | Slight slowdown |

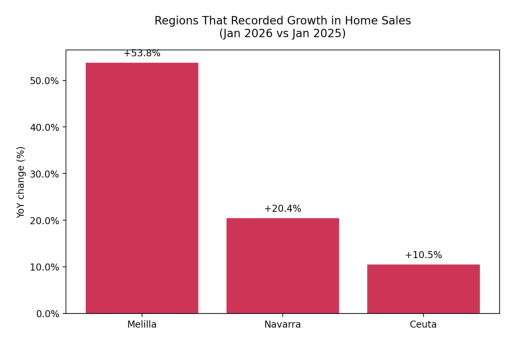

| Navarra | +20.4% | Strong growth |

| Ceuta | +10.5% | Moderate increase |

| Melilla | +53.8% | Highest growth in Spain |

Key Highlights:

- The steepest declines occurred in Canary Islands, Community of Madrid, Castilla-La Mancha, and Asturias.

- Conversely, Melilla, Navarra, and Ceuta recorded the strongest growth.

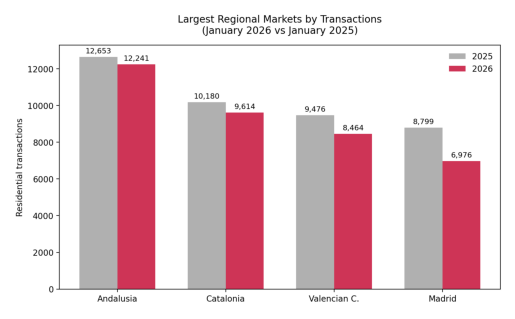

- Despite declines in some regions, Andalusia, Catalonia, Valencian Community, and Madrid remain the largest contributors to total transaction volumes. ([InfoConstrucción][1])

Residential Property Transactions by Autonomous Community (Jan 2026 vs Jan 2025)

| Autonomous Community / City | 2026 Transactions | 2025 Transactions | YoY Change |

|---|---|---|---|

| Andalusia | 12,241 | 12,653 | −3.2% |

| Catalonia | 9,614 | 10,180 | −5.6% |

| Valencian Community | 8,464 | 9,476 | −10.8% |

| Community of Madrid | 6,976 | 8,799 | −20.8% |

| Canary Islands | 3,214 | 4,150 | −22.7% |

| Castilla-La Mancha | 3,107 | 3,811 | −18.5% |

| Galicia | 2,908 | 3,123 | −6.8% |

| Castilla y León | 2,744 | 2,978 | −7.9% |

| Basque Country | 2,416 | 2,547 | −5.1% |

| Murcia | 1,954 | 2,031 | −3.9% |

| Aragón | 1,481 | 1,676 | −11.7% |

| Balearic Islands | 1,367 | 1,460 | −6.4% |

| Asturias | 1,123 | 1,330 | −15.5% |

| Navarra | 812 | 675 | +20.4% |

| Cantabria | 687 | 718 | −4.3% |

| Extremadura | 631 | 644 | −2.1% |

| La Rioja | 412 | 450 | −8.4% |

| Ceuta | 63 | 57 | +10.5% |

| Melilla | 61 | 40 | +53.8% |

Top 5 Regions by Growth and Decline (Jan 2026 vs Jan 2025)

| Category | Region | YoY Change | 2026 Transactions | 2025 Transactions |

|---|---|---|---|---|

| Top Growth | Melilla | +53.8% | 61 | 40 |

| Navarra | +20.4% | 812 | 675 | |

| Ceuta | +10.5% | 63 | 57 | |

| Top Decline | Canary Islands | −22.7% | 3,214 | 4,150 |

| Community of Madrid | −20.8% | 6,976 | 8,799 | |

| Castilla-La Mancha | −18.5% | 3,107 | 3,811 | |

| Asturias | −15.5% | 1,123 | 1,330 | |

| Valencian Community | −10.8% | 8,464 | 9,476 |

Coastal vs Inland Market Trends

Spain’s housing market shows clear differences between coastal and inland regions, with important implications for buyers and investors:

Coastal Markets

- High international demand, particularly from Northern European buyers.

- Popular regions: Costa del Sol, Costa Blanca, Balearic Islands, Canary Islands.

- Foreign buyers account for 20–40% of purchases in some municipalities.

- Price growth remains resilient even where transaction numbers have slightly declined.

- Lifestyle, tourism, and rental yield opportunities continue to attract investment.

Inland Markets

- Slower growth due to lower population density and limited foreign demand.

- Regions: Castilla y León, Extremadura, Castilla-La Mancha, parts of Aragón.

- More affordable housing options attract domestic first-time buyers.

- Transaction volumes are lower, but price stability offers long-term investment potential.

- Smaller markets like Navarra, Ceuta, and Melilla outperform national trends due to local demand surges and government incentives.

Summary: Coastal regions dominate headline numbers and international investment, while inland markets provide stability, affordability, and niche growth opportunities.

The NLS Conclusion

Spain’s early-2026 housing data indicates a transition to a more regionally differentiated market. Coastal and metropolitan regions are moderating due to affordability pressures, while smaller autonomous communities experience strong growth.

Mortgage lending remains robust, supporting underlying demand, but regional dynamics are increasingly decisive. Investors and developers should focus on areas where demand exceeds supply, particularly in major cities and coastal regions.

Overall, Spain’s property market is entering a phase of more sustainable and selective growth, with both challenges and opportunities defined by local conditions, financing trends, and regional market dynamics.