Why American Buyers Matter More Than Their Market Share Suggests

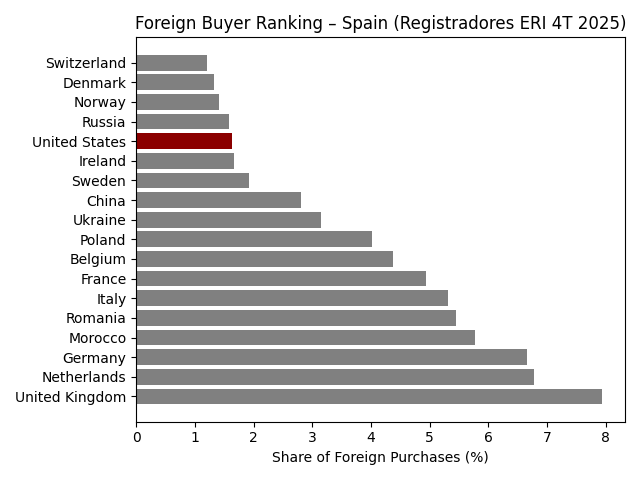

United States Share: ~1.64% of foreign purchases (Registradores ERI 4T 2025)

On paper, the United States is a minor player in Spain’s foreign property market.

But market influence is not determined by percentage alone.

In property markets – especially in premium ecosystems – where capital concentrates matters more than how much capital exists.

And this is where the American 1.6% becomes strategically relevant.

Full Foreign Buyer Ranking (Registradores ERI 4T 2025)

| Rank | Country | Share (%) |

|---|---|---|

| 1 | United Kingdom | 7.93% |

| 2 | Netherlands | 6.77% |

| 3 | Germany | 6.65% |

| 4 | Morocco | 5.78% |

| 5 | Romania | 5.45% |

| 6 | Italy | 5.32% |

| 7 | France | 4.93% |

| 8 | Belgium | 4.38% |

| 9 | Poland | 4.01% |

| 10 | Ukraine | 3.15% |

| 11 | China | 2.81% |

| 12 | Sweden | 1.92% |

| 13 | Ireland | 1.67% |

| 14 | United States | 1.64% |

| 15 | Russia | 1.58% |

| 16 | Norway | 1.41% |

| 17 | Denmark | 1.33% |

| 18 | Switzerland | 1.21% |

This table clarifies the structural reality:

The United States ranks 14th in transaction share.

And yet — ranking does not equal influence.

Volume vs Gravity

Let’s distinguish two different forms of market power:

Volume Power

– Drives absorption

– Anchors liquidity

– Stabilises mid-market pricing

– Sustains transaction flow

Gravity Power

– Concentrates in high-value nodes

– Influences price ceilings

– Elevates documentation standards

– Shifts seller expectations

The UK, Netherlands, Germany and Morocco exert volume power.

The United States exerts gravity power.

American demand clusters in:

- Prime Barcelona districts

- Madrid’s central high-value neighbourhoods

- Marbella’s upper villa market

- Mallorca prestige corridors

These are not broad absorption markets.

They are benchmark markets.

When benchmarks shift, ecosystems shift.

The Currency Amplifier

Currency does not just alter purchasing power.

It alters perception of value.

When the dollar strengthens against the euro:

- Spain feels discounted

- Risk perception drops

- Comparative confidence rises

A €3M villa in Marbella feels different when benchmarked against:

- $6–8M Miami waterfront

- Manhattan luxury inventory

- California coastal pricing

Americans do not compare Spain internally.

They compare Spain globally.

This global benchmarking injects a different pricing psychology into prime corridors.

Even at 1.6%, this psychology influences negotiation dynamics.

Behavioural Impact on Ecosystem Standards

American buyers typically originate from MLS-dominated environments.

They are accustomed to:

- Single source of listing truth

- Clear representation structure

- Document transparency

- Public pricing histories

Spain’s multi-agency duplication model creates friction for this profile.

When a property appears:

- Three times

- With three prices

- Under three agents

It does not signal competition.

It signals governance weakness.

This behavioural friction has two consequences:

- Some U.S. buyers disengage.

- Some agents elevate their standards to convert them.

Over time, standards rise in premium nodes.

That is ecosystem influence without volume dominance.

Strategic Capital vs Climate Capital

Compare motivations:

Northern Europe (Sweden, Norway, Netherlands)

→ Climate-driven seasonal living

Morocco, Romania

→ Structural settlement and family consolidation

United States

→ Portfolio diversification

→ Lifestyle optionality

→ Cross-border capital positioning

→ Education planning

→ Long-horizon wealth strategy

Strategic capital behaves differently.

It demands:

- Legal precision

- Tax advisory alignment

- Transactional governance

- Long-term asset logic

This increases professional scrutiny in segments where Americans operate.

The Premium Corridor Multiplier

If American demand concentrates in prime and luxury bands,

their 1.6% may represent a higher proportion of total foreign capital value than transaction volume suggests.

Volume share ≠ capital share.

Premium-weighted segments amplify influence.

Competitive Benchmark Pressure

American buyers evaluate Spain against:

- Portugal

- Southern France

- Italy

- Florida

- California

If Spain’s listing ecosystem appears opaque, capital reallocates.

If Portugal appears more structured, it absorbs governance-sensitive demand.

This competitive pressure affects:

- Agent behaviour

- Platform structure

- Professionalisation of premium nodes

The presence of governance-sensitive buyers forces ecosystem maturity.

Even at 1.6%.

Influence Through Expectation Signalling

Markets adapt to their most demanding participants.

In premium segments, Americans are among the most demanding in terms of:

- Documentation clarity

- Representation transparency

- Compliance certainty

- Legal predictability

That expectation signalling affects:

- Developers

- High-end agencies

- Luxury brokers

- Marketing presentation standards

When premium participants demand structure, structure spreads.

What 1.6% Is Not

It is not:

- A volume stabiliser

- A rental-driven mass segment

- A climate-only migration cohort

- A mid-market liquidity engine

It is selective, concentrated, governance-sensitive capital.

That is a different kind of influence.

Why This Matters for Spain’s Future Positioning

If Spain wants to compete as:

- A premium European destination

- A wealth-preservation jurisdiction

- A structured international market

It must satisfy governance-sensitive buyers.

These segments do not define market size.

They define market credibility.

The NLS Structural Angle

In a fragmented listing environment, duplication erodes confidence.

For governance-sensitive segments:

Clarity accelerates commitment.

The NLS framework addresses precisely the friction points that matter most to:

- American buyers

- Swiss buyers

- Premium international capital

By:

- Verifying property identity

- Reducing duplication

- Clarifying representation

- Making structure visible

NLS does not increase the American share.

It improves the American conversion environment.

And improving conversion in premium segments has disproportionate impact.

Conclusion: Small Share, Strategic Signal

1.64% is not a headline number.

It is a diagnostic indicator.

It tells us:

- Where governance expectations are rising

- Where pricing psychology is globally benchmarked

- Where ecosystem professionalism matters most

The United States may rank 14th in share.

But in premium corridors, it acts as a standards multiplier.

And standards multipliers shape markets long before their percentage share grows.